|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

||

|

||

|

|

|

|

Best Mortgage Refinance Cash Out: Key Insights and TipsRefinancing your mortgage can be a strategic way to access extra funds by leveraging your home's equity. But with so many options, choosing the best mortgage refinance cash out can be daunting. Here, we explore the key considerations and common pitfalls to help you make an informed decision. Understanding Cash-Out RefinanceA cash-out refinance involves replacing your existing mortgage with a new one, for a larger amount, allowing you to take the difference in cash. This can be beneficial for consolidating debt, funding home improvements, or covering unexpected expenses. Benefits of Cash-Out Refinance

Drawbacks to Consider

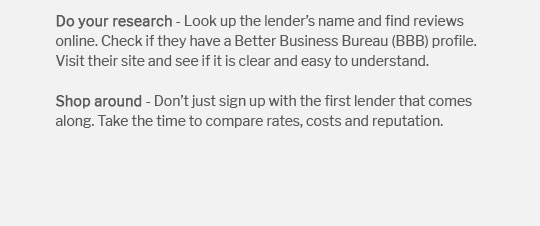

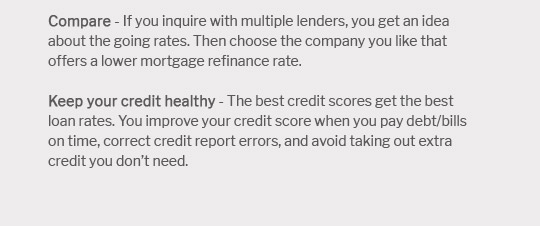

Common Mistakes to AvoidWhen considering a cash-out refinance, avoid these common errors to ensure the process benefits you: Not Shopping AroundFailing to compare rates from multiple lenders can cost you. Explore different offers to find the best terms. If you're considering refinancing your second home, learn more about options like the FHA streamline refinance second home. Ignoring Total Loan CostsFocus not only on interest rates but also on the total cost of the loan, including fees and closing costs. Overestimating Home ValueAn inflated sense of your home's value can lead to loan denial or less favorable terms. Use a professional appraisal to get an accurate assessment. Making the Right DecisionEnsure a cash-out refinance aligns with your financial goals. Consider working with a financial advisor to assess your situation. If you've had financial setbacks, explore refinancing options that accommodate unique situations, such as FHA streamline refinance with late payments. FAQs

By carefully evaluating your options and avoiding common pitfalls, you can effectively utilize a cash-out refinance to meet your financial needs. https://www.ramseysolutions.com/real-estate/cash-out-refinancing?srsltid=AfmBOooih_PbZ3ZqK3ab67Vp8kVIwR8st37cJqX6HcPm1reN4KpBUpBX

But instead of shortening your mortgage term or lowering your interest rate, you get a bigger mortgage that also gives you access to cash. Here ... https://www.investopedia.com/mortgage/refinance/cash-out-vs-mortgage-refinancing-loans/

The mortgage's size remains the same; you trade your current mortgage terms for newer (presumably better) terms. In contrast, in a cash-out refinance loan, the ... https://www.cnbc.com/select/cash-out-refinance-vs-heloc-what-to-know/

A cash-out refinance replaces your existing mortgage with a new, larger one. A HELOC is a second mortgage with its own rate and term.

|

|---|